San Diego Real Estate Market 2026: Key Insights

Real Estate, San Diego Housing Market 2026

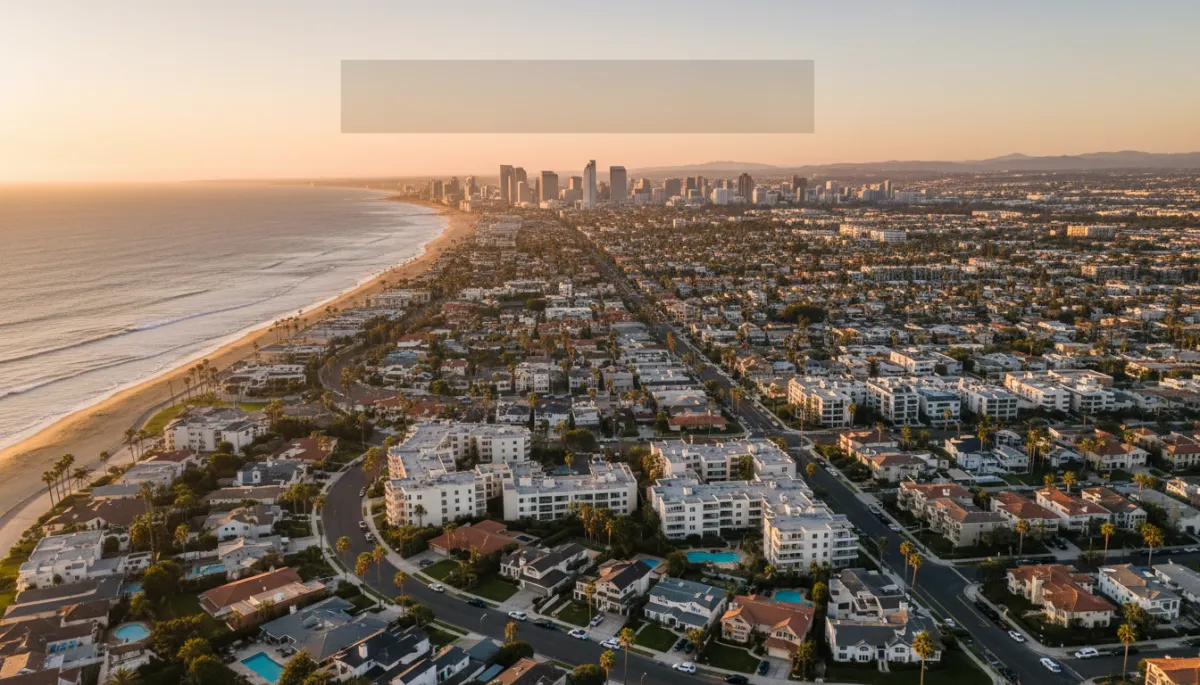

San Diego Real Estate Market Overview 2026: What Local Homeowners Need to Know

The San Diego and Chula Vista housing markets are shifting in 2026—but not in a simple “up or down” way. Detached homes, condos, and individual neighborhoods are moving at very different speeds. As a homeowner, understanding these nuances is essential for decisions about selling, refinancing, or holding your property over the next 12–24 months.

The State of the San Diego Market in 2026

As of spring and early summer 2026, San Diego County remains one of the most expensive housing markets in the country, yet price growth has cooled and become more uneven. Countywide, the median sale price across all property types hovers around $930,000, with some sources such as Redfin placing March 2026 closer to $950,000 and Homes.com reporting $925,500 in April.1 Year-over-year, that translates to a modest decline of roughly 1–6%, depending on the data source and time frame you use.

Homes are taking slightly longer to sell—around 25–36 days on average—yet well-priced listings, particularly single-family homes in desirable neighborhoods, still attract multiple offers. In short, this is no longer the frenzied market of 2021–2022, but it is far from a buyer’s market. Instead, 2026 is best described as a selectively competitive environment, where property type, price point, and neighborhood matter more than ever.

Key Trends Shaping 2026: A Two-Tier Market

The defining feature of 2026 is a clear split between detached homes and attached properties. Detached single-family homes remain in high demand and short supply, while condos and townhomes are seeing softer prices and longer marketing times.2 Remote work, lifestyle preferences for yards and more space, and limited buildable land all continue to favor single-family homes.

- Single-family strength: Modest price gains, low inventory, and multiple-offer situations in many neighborhoods.

- Condo softness: Price declines, especially in areas with high HOA dues or dense new construction.

- Micro-market divergence: Neighborhoods like North Park and parts of East Chula Vista are outperforming, while others, including Bonita and West Chula Vista, have cooled.

Median Home Prices: San Diego and Chula Vista Snapshot

For detached single-family homes countywide, recent reports place the median around $1,060,000–$1,100,000, up roughly 1–2.5% year-over-year.1,2 Condos and townhomes, by contrast, sit near $632,000–$660,000, down 3–4% from a year ago. The gap of roughly $430,000–$450,000 between those segments underscores how differently they are behaving.

Within the city of San Diego, some urban neighborhoods are outperforming the county average. North Park, for example, saw its median single-family price climb to about $1.31 million, a striking 13.9% increase year-over-year, with homes selling in roughly 12 days and often above list price.3 In contrast, parts of South Bay tell a more mixed story:

- Bonita: Median single-family prices around $1.325 million, but down nearly 15.9% year-over-year, signaling a meaningful correction.3

- East Chula Vista: Median near $1.125 million, up about 6.3% year-over-year, with days on market in the low 30s.3

- West Chula Vista: Median around $828,600, down roughly 3.1%, but still relatively low inventory at about 1.6 months of supply.3

South Bay neighborhoods show mixed trends, with some areas rising and others correcting.

Inventory Levels: Still Tight, but Easing at the Edges

Inventory remains below what economists consider a “balanced” market. Single-family homes sit at roughly 1.7–1.9 months of supply, while condos and townhomes offer about 2.5–2.8 months.1,2 A truly balanced market is closer to six months, so San Diego is still structurally undersupplied—especially for detached homes.

The shortage is most acute in the $700,000–$950,000 “entry-level” single-family bracket, where one analysis found a 50% year-over-year drop in available listings heading into the 2026 spring season.4 For many households in San Diego and Chula Vista, that translates to fewer realistic options if they hope to move up or downsize within the county.

Interest Rates and Affordability Pressures

Mortgage rates in early 2026 have hovered in the 6.1%–6.7% range, with some forecasts suggesting a possible drift toward the mid-5% range later in the year.5 While that would be welcome relief compared with 2023 peaks, it is still significantly higher than the ultra-low rates many current homeowners locked in during the pandemic years.

Affordability remains a serious challenge. One Axios report estimates that only 1.6% of homes in San Diego are affordable to a typical household, and buyers would need an income of roughly $221,900 to comfortably purchase the median-priced home.6 This affordability squeeze is a key reason many would-be move-up buyers are “rate-locked” in place, contributing to ongoing inventory shortages.

What This Means for Local Homeowners in San Diego and Chula Vista

For homeowners, 2026 presents both risks and opportunities, depending on your goals, location, and property type.

- If you own a single-family home in a high-demand neighborhood—such as North Park, parts of East Chula Vista, or coastal areas—you are likely still in a strong equity position. Limited supply and steady demand mean you can sell, provided you price strategically and present the home well. Many sellers in these pockets are still seeing multiple offers and favorable terms.

- If you own a condo or townhome, especially in areas with higher HOA dues or abundant new construction, expect more negotiation. Buyers today are value-conscious and have options. Upgrading finishes, addressing deferred maintenance, and pricing in line with recent sales—not peak 2022 prices—will be critical to a successful sale.

- If you plan to stay put, current conditions still work in your favor: low vacancy rates and a large pool of would-be buyers support long-term values, even if year-to-year appreciation is modest. Many owners are choosing to remodel, add ADUs, or consider future multigenerational living rather than trading their low-rate mortgages for higher payments elsewhere.

Looking ahead, most forecasts call for flat to modest price growth—roughly 0–5%—through the rest of 2026, with continued strength in well-located single-family segments and more variability in condos and softening submarkets.5 For San Diego and Chula Vista homeowners, the most prudent approach is to think in terms of a three- to seven-year horizon, rather than trying to time short-term market swings.

Next Steps: How to Position Your Property in 2026

Whether you are in San Diego proper or in Chula Vista, your best move is to ground decisions in hyper-local data. That means reviewing recent sales on your block, understanding how many comparable homes are currently listed, and factoring in your mortgage rate, tax basis, and lifestyle needs. A professional valuation and a conversation with both a lender and a real estate advisor can clarify whether 2026 is the right time to sell, refinance, or simply hold and improve what you already own.

In a market as segmented and supply-constrained as San Diego’s, informed homeowners are the ones who make the most of shifting conditions. Understanding the current state of prices, inventory, and interest rates is the first step toward making confident, well-timed decisions for your household.

BOOK AN APPOINTMENT WITH US TODAY!

What Our Clients are Saying

Martin Barros